Compliance Management 101: The Basics

If your employees struggle to understand and manage your corporate compliance obligations, they’re not alone. Compliance risk management, as part of an overarching GRC framework, can be a daunting task. Rules and regulations are often moving targets, with systems, processes and actions needing an element of reactivity that can be difficult to manage.

But compliance management doesn’t have to be overwhelming, scary or negative. Breaking it down to its basics–what is corporate compliance, what benefits does it bring and how to implement a plan, tools, checks and controls–will both educate your employees and protect your organization.

What is corporate compliance?

Corporate compliance is an important element of your business. At its most basic level, a good compliance process ensures that you never find yourself breaching your regulatory requirements, or facing the organizational risks that could arise from a breach. Any breach could have far-reaching consequences, including lawsuits, fines and even criminal penalties.

resize.png?width=512)

What is compliance management?

Every business, in every industry, has specific rules, laws and regulations with which it must comply. These standards are sometimes set by federal or state government agencies, industry oversight groups or other regulatory bodies or internally by the organization. These requirements are referred to as corporate compliance, or sometimes as governance, risk management and compliance (GRC compliance). Regardless of the terminology, non-compliance can be a risk to your ability to operate your business and achieve your business outcomes and desired goals.

Compliance management then is simply the process for managing your compliance requirements. In short, it’s all the systems and protocols that ensure your organization never faces the potential risks of non-compliance.

Benefits of corporate compliance

There are benefits to being a compliant organization that go far beyond mitigating negative consequences. Compliant organizations tend to have an excellent company reputation. They are on the forefront of industry innovations and trends. They have more efficient, replicable and streamlined processes. And they empower employees to take ownership of their decisions and rapid actions based on those decisions.

Benefits:

- Avoid the negative consequences of breaches

- Remain on the forefront of industry innovations and trends

- Retain an excellent company reputation

- Boost employee morale

- Boost employee efficiency

- Increase overall productivity

- Improve organizational standardization

- Increase transparency

What is a compliance management plan?

Your compliance management plan is essentially the framework that you put in place to identify, monitor and manage your compliance risks and obligations. It starts with identifying your obligations and completing a risk assessment. Then you’ll need to incorporate systems, policies and procedures to backstop those risks and obligations. And finally you’ll need to ensure that the right stakeholders have access to timely and accurate reports and information.

How to create a compliance management plan

Step 1: Identify your obligations.

The first step is identifying your obligations. Every industry and organization will have its own unique compliance requirements. This includes any duties and obligations towards the government, employees, investors or third parties.

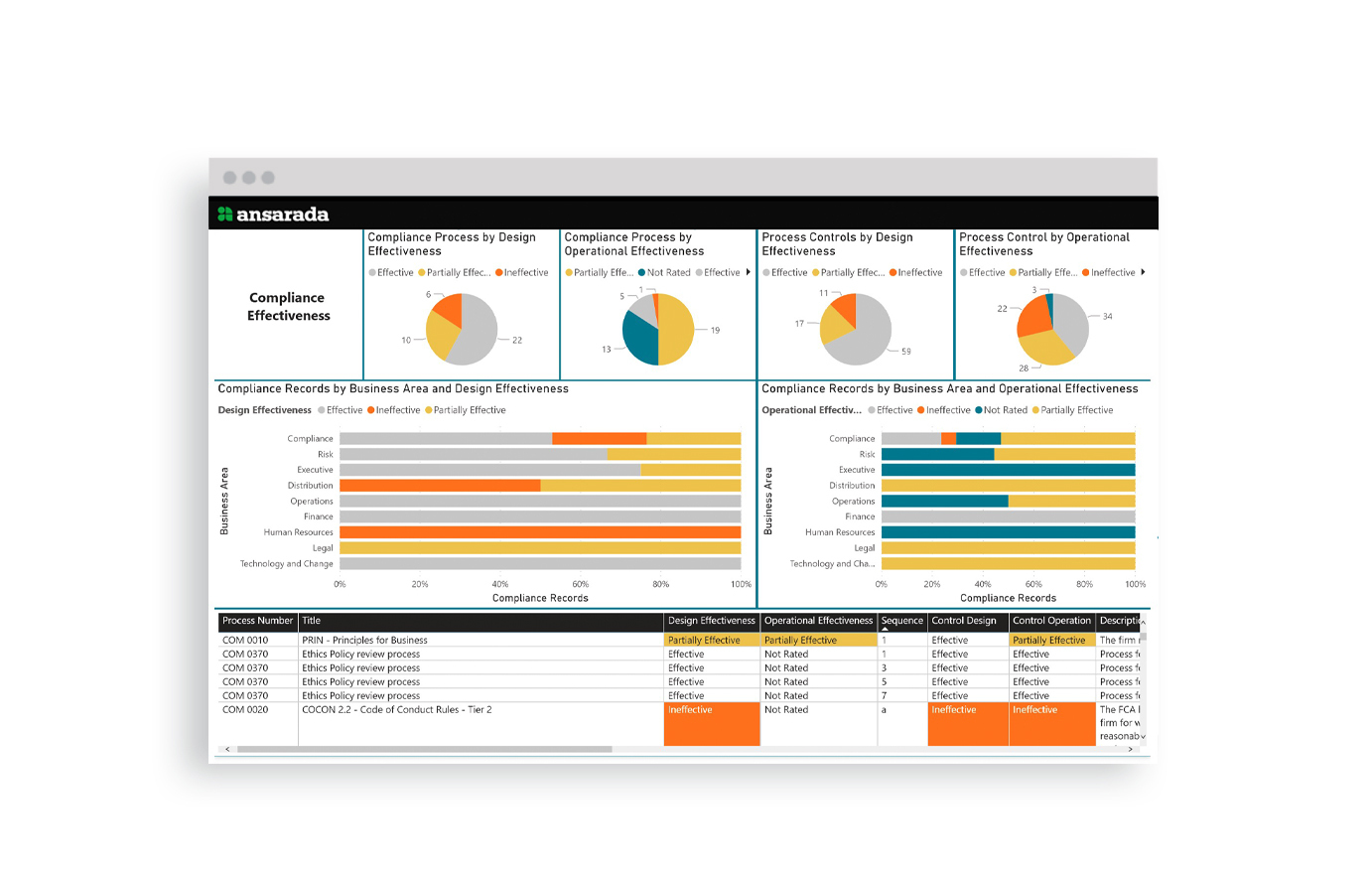

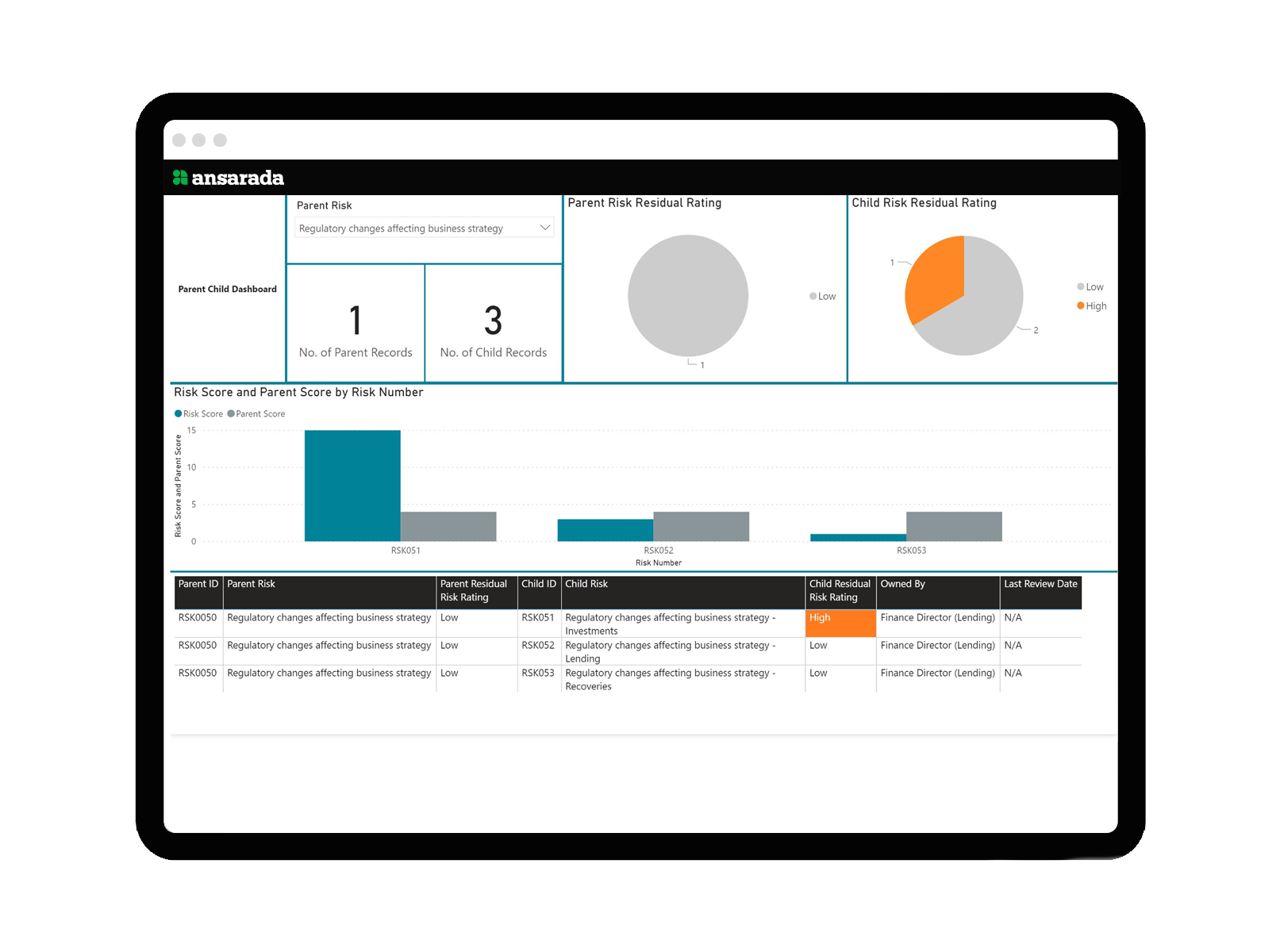

Once you’ve identified these obligations, you’ll need to develop a system for regularly checking for new or updated requirements that you may need to respond to or implement. This is where an automated compliance management system like Ansarada GRC, can be a corporate game changer. These kinds of systems allow you to effectively manage and cross-track obligations across relevant legislation, as well as third-party and internal requirements.

Step 2: Undertake risk assessments.

Step two is to complete a compliance risk assessment (or CRA). A CRA is simply the process of identifying the risks that your specific business and industry may face. When it comes to your corporate and regulatory compliance you will be identifying risks related to legal compliance, data protection, internal policies and procedures, internal conduct and any other compliance-related matters.

Your CRA is an important step to creating a strong compliance management plan. It allows you to find the risks within your business and determine their level of importance and impact. Then you can begin to implement systems and formulate actions to ensure you’re managing these risks effectively.

Step 3: Incorporate compliance policies and procedures.

Once you understand your obligations and have identified your risks, it’s time to develop and implement the right policies and procedures. This is where things can get a little tricky. There are many options–from internally managed spreadsheets to Ansarada GRC and each will give you a varying level of comfort.

Regardless of your choices here, you’ll need to implement policies and procedures that:

- Ensure you’re meeting your obligations.

- Track changes and updates to those obligations.

- Manage any identified risks.

- Set the standards for organizational compliance.

- Assign ownership and responsibility to employees and teams.

- Keep records of your compliance history for auditing purposes.

- Create customized reports on your compliance history, progress and future obligations.

- Are regularly available to be reviewed, assessed and updated to react to changes and developments internally and externally.

Step 4: Report.

With any corporate compliance management process, reporting is vital. It helps you understand your compliance environment. It reassures board members, the management team and external stakeholders that your obligations are being met. It helps you identify inefficiencies and remedy them. And it helps you to be prepared for all your internal and external audits.

A comprehensive software system can help you develop, automatically generate and even distribute customized reports to keep you on the cutting edge of compliance management in your industry.

Top compliance challenges in the 2020s

The last couple of years have had a big impact in the compliance world. The COVID and post-COVID workplace, the increasing frequency of cyber crime and fraud and the growing trends around psychological safety are just some of the changes that businesses and their compliance teams have had to adapt to meet.

COVID and Post-COVID workplace

The global pandemic has seen many businesses’ operating models disrupted and perhaps changed forever. There are new risks associated with employees who are at a physical and psychological distance from their team. Without a doubt, remote oversight needs to form a large part of risk management in the immediate future.

Climate change

Climate change remains a big part of the compliance world. Countries are beginning to (or have already) introduced mandatory climate risk disclosures for some industries. And there are often financial, legal, operational and reputational risks from a regulatory and governance perspective.

Cyber security

Almost all businesses and industries will have some sensitive or valuable information in their possession. And this means they are at risk of cyber attacks. Many federal, state and industry regulators have introduced requirements and guidance that help entities to manage the risk of potential malicious activities. These regulations are being updated continuously to respond to the growing sophistication of this type of crime.

Fraud

According to PwC’s Global Economic Crime and Fraud Survey 2020, 47% of business respondents had been the victim of at least one form of fraud in the previous two years. Worse, the average number of fraudulent activities per organization was six. These generally included “customer fraud, cybercrime, asset misappropriation, and bribery and corruption”. The total cost of these crimes to the businesses was over $42 billion.

Fraud (continued)

This rapidly increasing level of fraudulent activity is a heavy risk for businesses. Employees must be adequately trained on all fraud risk and incorporate this into their compliance management processes both on a micro and macro level.

Psychological safety

Employee health and mental wellbeing is an important part of any organization. A rising trend–related to health and wellbeing–is psychological safety. This requires a business to cultivate a healthy culture where people aren’t afraid to speak up when mistakes are made. Higher psychological safety results in better reliability and performance, and improved governance, compliance and controls.