M&A growth rates normalize after recent bumper years

New M&A deals commencing decreased by 7% this quarter but increased by 10% compared to the previous corresponding period. Over the whole financial year, M&A activity was down 21%.

By AnsaradaTue Aug 22 2023Mergers and acquisitions, Due diligence and dealmaking, Industry news and trends, Virtual Data Rooms

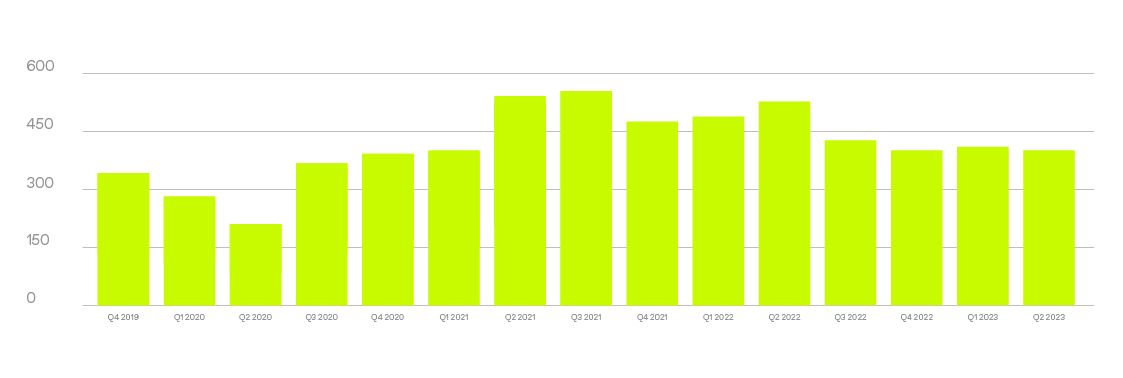

The latest Deal Indicators M&A numbers paint a picture of stabilization after the bumper post-COVID years and the megadeals of 2021. As shown by the below chart, M&A deal volumes are steadily returning to the typical growth levels we would expect. Volumes have fallen back toward pre-pandemic levels, but stronger.

Open M&A Rooms; Source: Ansarada

In their Global M&A Industry Trends: 2023 report, PwC predicts a healthier level of mid-market deals to dominate M&A activity, driving strategic growth agendas. Their own data aligns closely with Indicators – while closed M&A deal volumes declined by 4% in the first half of 2023, they remain above pre-pandemic levels, showing a stabilization and steady-paced growth in M&A activity. Much of the activity is expected to be driven by middle and lower markets, which have stayed solid despite the slowdown in larger M&A deals.

It’s not necessarily all smooth sailing though. Bain & Company calls the current M&A market ‘lethargic’ and ‘weird’, characterized by ups, downs, and mixed signals.

‘Deal valuations have fallen dramatically, but hover above a typical downturn trough. Central banks continue to raise interest rates, yet an inverted bond market suggests a coming reversal. Layoffs have accelerated, but the hiring market remains resilient. Inflation has slowed, but persists. The much-anticipated recession hasn’t officially arrived, yet executives are deploying downturn playbooks with a renewed focus on cost discipline.’ (Bain & Company)

Despite the perceived sluggishness in M&A activity, teams are actively preparing for the future by focusing on strategic repositioning, business model changes, and preparing for more complex due diligence processes, so they can be ready to act quickly when the market ramps up again.

The latest Deal Indicators M&A numbers paint a picture of stabilization after the bumper post-COVID years and the megadeals of 2021. As shown by the below chart, M&A deal volumes are steadily returning to the typical growth levels we would expect. Volumes have fallen back toward pre-pandemic levels, but stronger.

Signs of a potential booming M&A Asian market

There are already signs of an M&A boom in Asia, particularly in the Oil & Gas market.

According to research conducted by Rystad Energy, it is predicted that there will be a significant increase in M&A deals in Southeast Asia, involving more than $5 billion worth of assets that will become available for acquisition. The majority of these opportunities are located in Indonesia, with assets valued at around $2 billion being offered for sale. Following Indonesia are Malaysia and Vietnam, where approximately $1.4 billion and $1 billion worth of assets are respectively up for sale.

So far in 2023, around $700 million worth of deals have already been finalized in the region. This marks the most active start to upstream M&A activities in Southeast Asia since 2019.

M&A as a catalyst for transformation

Dealmakers may have kicked off 2023 with a cautious outlook due to recession fears and rising interest rates, but inflation is slowing, and opportunities are starting to arise out of dynamic market conditions. The companies that thrive in such an environment will be those executing bold M&A strategies focused on transformative business models.

Businesses will explore new avenues of value creation that aren’t purely financial, but are means of driving profit through purpose. In their mid-year update, PwC writes that previously lesser-considered levers, like energy efficiency, green tax credits and sustainable financing, are becoming more important for deal success. The importance of considering sustainability performance in M&A is at a peak.

M&A will play a critical role for companies who are ready to make a shift and build resilience through access to new capabilities, talent, or markets – with sustainability, AI and digital transformation at the top of the 2024 agenda.